Up Nearly 60% in 2025, Is It Too Late to Buy Snowflake Stock?

/An%20image%20of%20the%20Snowflake%20logo%20on%20a%20corporate%20office_%20Image%20by%20Grand%20Warszawski%20via%20Shutterstock_.jpg)

Snowflake (SNOW) has emerged as one of the most closely watched names in enterprise software and cloud computing. With a market capitalization of nearly $67 billion, it has quickly evolved with thousands of enterprise customers, rapidly expanding use cases, and increasing relevance in the artificial intelligence (AI) ecosystem.

Snowflake’s recent second quarter of fiscal 2026 showed the strength of its business model, the long-term sustainability of its customer relationships, and its growing role in the rapidly changing world of data and AI.

SNOW stock is up 56.1% year-to-date and nearly 120% over the past 52 weeks. Is there any room left for Snowflake to run here?

Focus on Simplicity and Customer Value Is Driving Growth

Snowflake is a cloud-based data platform that allows businesses to store, manage, and analyze large amounts of data. By consolidating diverse data sources into a unified environment, Snowflake enables customers to move faster, make better decisions, and reduce the friction that traditionally slows large enterprises. During the Q2 earnings call, CEO Sridhar Ramaswamy emphasized that this is exactly why customers like Booking.com (BKNG), Hyatt Hotels (H), and InterContinental Exchange (ICE) chose Snowflake.

In the second quarter of fiscal 2026, product revenue increased by 32% year on year to $1.09 billion. The company’s remaining performance obligations (RPO), a key indicator of future revenue, increased 33% year on year to $6.9 billion, while the net revenue retention rate (NRR) was a strong 125%. These figures reflect both strong new customer acquisition and increased usage among existing clients.

While many software companies are experiencing growth slowdowns, Snowflake’s ability to maintain high growth while aggressively pushing innovation is admirable. The company now has over 12,000 customers, including 654 clients who generate more than $1 million in annual revenue, indicating strong adoption at the high end of the market.

However, its push for innovation has weighed on profitability. Snowflake reported a net loss of $0.89 per share in Q2. Its financial discipline resulted in an adjusted product gross margin of 76.4%. The company also generated adjusted free cash flow of $67.8 million.

Importantly, the company expects free cash flow to increase significantly in the second half of the year, fueled by large renewals and deal volume already in the pipeline.

AI at the Center of Snowflake’s Growth Story

AI has quickly become a key driver of Snowflake’s business. The company has integrated AI into its data cloud, introducing Snowflake Intelligence, which enables users to query structured and unstructured data using natural language.

Management acknowledged that AI influenced nearly 50% of new customer wins in Q2, and that 25% of all Snowflake workloads now include AI use cases. Snowflake’s AI capabilities are used by more than 6,100 accounts each week. Snowflake is also integrating AI natively into its workflows. Cortex AI SQL enables customers to run AI models directly inside Snowflake using SQL, eliminating the need for costly and risky data movement.

Snowflake ended the quarter with $4.6 billion in cash and investments, giving it plenty of room to continue investing in growth while navigating potential macroeconomic challenges.

Is SNOW a Buy on Wall Street?

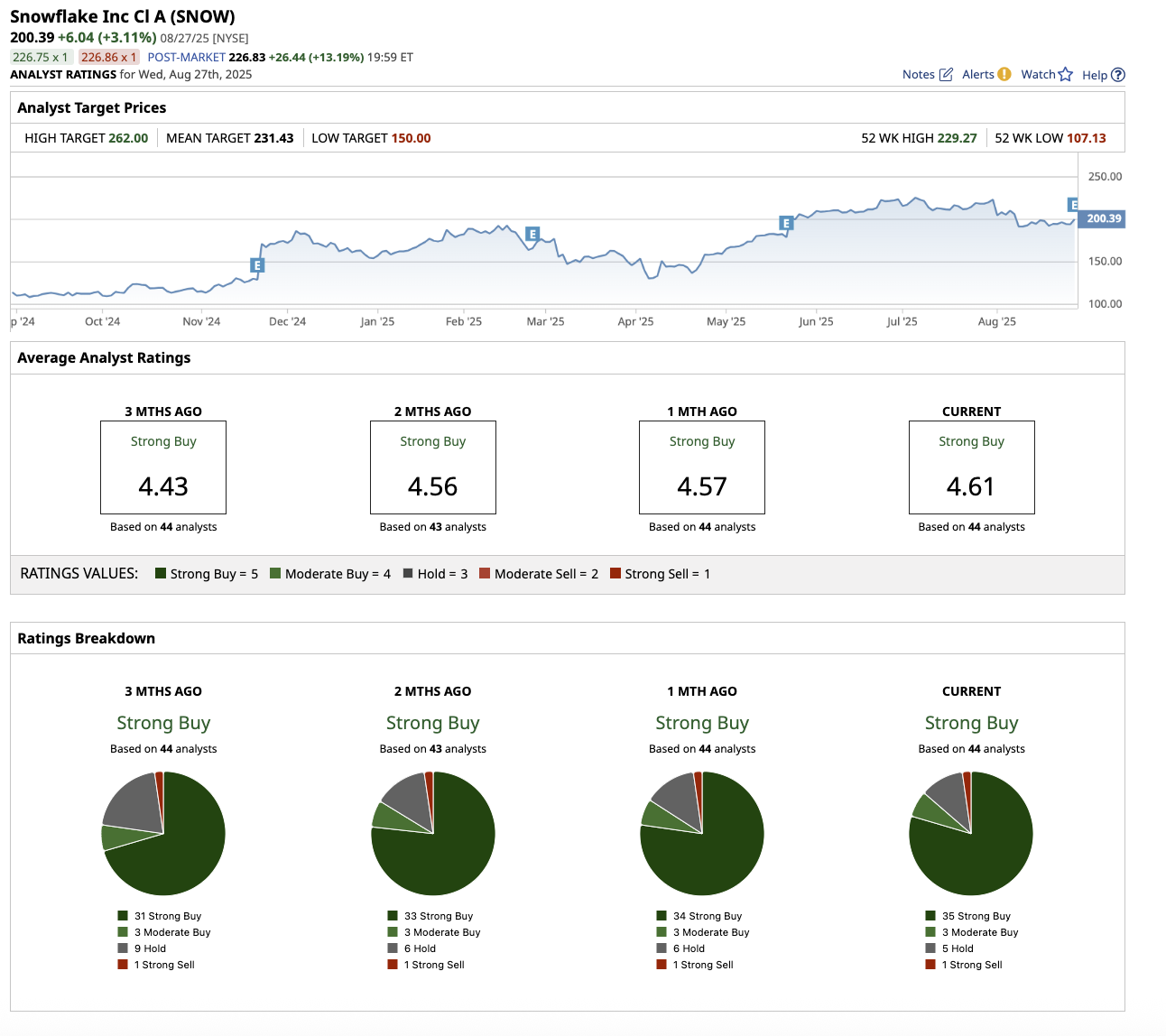

Overall, Wall Street has rated SNOW stock a “Strong Buy” even though it is not profitable, reflecting trust in the company’s long-term potential.

Out of the 44 analysts covering SNOW stock, 35 have rated it a “Strong Buy,” three suggest a “Moderate Buy,” five rate it a “Hold,” and one recommends a “Strong Sell.” The stock’s average target price of $231.43 is below its current trading price how.

However, it has a high target price of $262, which suggests the stock could gain as much as 9% over the next 12 months.

The Bottom Line on SNOW stock

Snowflake’s bull case focuses on its unique position at the crossroads of data and AI, its high-margin recurring revenue model, and its long adoption runway. However, some are concerned about its lack of profitability, competitive threats from hyperscale cloud providers, and the risk of growth deceleration as the company scales.

Overall, I believe that with product revenue accelerating, customer adoption deepening, and the success of its AI-first strategy, Snowflake has a massive opportunity ahead. SNOW may present an appealing opportunity for long-term investors with a high risk tolerance.

On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.